by Dylan Kinny, MLR Development Coordinator

Happy Holidays!

As the season of generosity is upon us once again, there are big changes on the horizon when it comes to charitable giving and your taxes. The new federal tax law passed this summer (2025) will change how you choose your tax deductions and deduct charitable gifts as an individual or business.

The Association of Fundraising Professionals has written some great articles about this that I will link below.

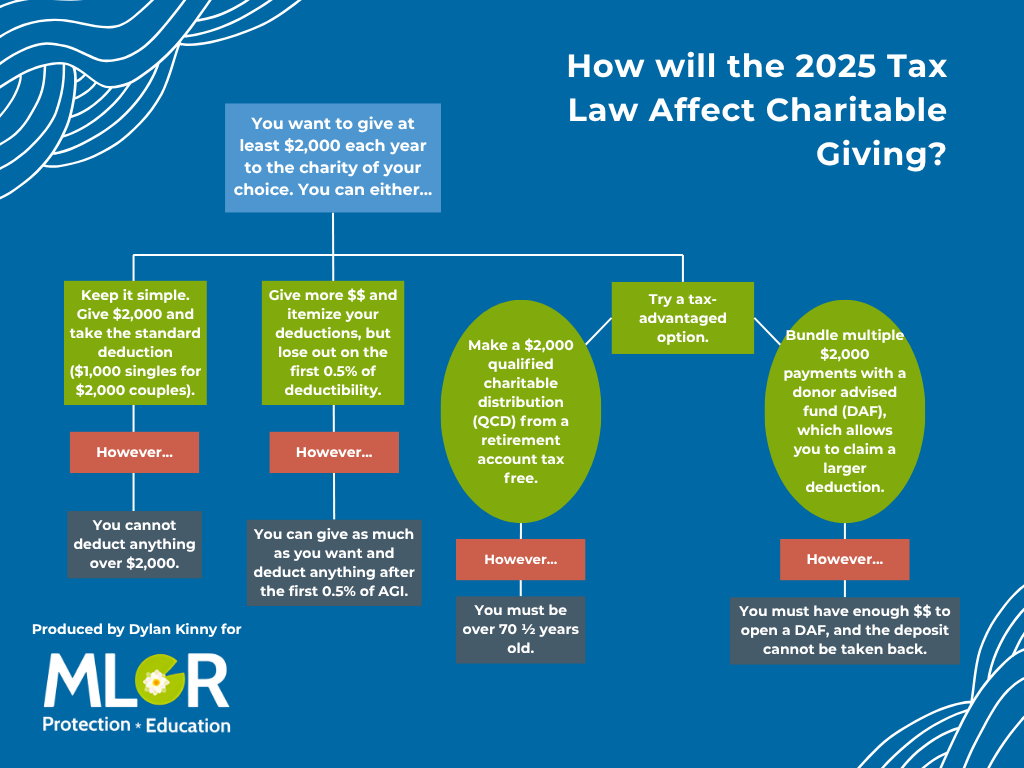

There’s good news for you! “Regardless of income or gift size, all taxpayers will be able to deduct charitable giving from their federal taxes. The new tax law brings back and expands upon the universal charitable deduction (UCD), which was included in the 2020 CARES Act, and makes it permanent. This allows those taking the standard deduction to deduct $1,000 for individuals or $2,000 for couples” (Association of Fundraising Professionals, 2025). This makes charitable giving more equitable, because anyone can get a tax deduction for making charitable gifts.

Bottom line: single filers who donate $1,000 or less and joint filers who donate $2,000 or less can keep it simple and take the UCD.

Unfortunately, for those of you who itemize your deductions each year, you will lose the deductibility of the first 0.5% of your Adjusted Gross Income (AGI) from charitable contributions. If you’re earning $200,000, that’s the first $1,000 of giving. At $800,000, it’s the first $4,000.

Additionally, for corporations, the first 1% of Adjusted Taxable Income won’t be deductible and the cap is at 10%. Basically, smaller gifts from corporations will become less tax-efficient in 2026. However, if business sector sponsorships can be described as marketing, they can be classified as business expenses and those expenses could be tax deductible. (Consult IRS Section 513(i) for an explanation of what constitutes “marketing.”)

For those who itemize, there is still good news.

Donor-Advised Funds (DAFs) will help high-AGI donors sidestep the new 0.5% deductibility loss every year if they bundle multiple years of giving into one tax year.

- For example, if you and your spouse give $2,000 each year to Minnesota Lakes and Rivers Protection and Education (MLR P&E), you would usually take the standard deduction. However, by bundling four years of contributions into one and starting a DAF with that money, you would be able to deduct all four years of charitable contributions on your 2025 taxes ($8,000 in this example). Then over the next four years, that $2,000 is annually “granted” from the DAF to MLR P&E or any other 501(c)3.

- If you do this in 2025, that eliminates the impact of the 0.5% floor altogether, at least for the next few years. With Minnesota Lakes and Rivers Protection and Education (MLR P&E), you can give directly from a Donor Advised Fund (DAF).

- The SALT (State and Local Tax) deduction cap has been raised to $40,000 for those with AGI under $500,000. This may prompt more donors to itemize again—especially in high-tax states.

- Qualified Charitable Distributions (QCDs) from retirement accounts will remain one of the most tax-efficient giving tools available. This allows donors 70½ or older to donate directly from their IRA, up to $108,000 per person in 2025 and $115,000 in 2026 without it counting as taxable income. You can do this by giving to Minnesota Lakes and Rivers Protection and Education (MLR P&E), our 501(c)3 side.

Bottom line: this new AGI floor might cause confusion, but it can be avoided by giving from tax-advantaged vehicles like IRAs and Donor Advised Funds. Giving this way is not just advantageous from a tax perspective, it’s also easier once you initiate the process with your financial advisor.

This can be complex, so if you have questions about how it may affect you, take the time to consult your financial advisor. The information provided here is for educational purposes only and is not intended as financial or legal advice.

If you’re interested in making a contribution to Minnesota Lakes and Rivers Protection and Education (MLR P&E), we have a helpful guide that walks you through the process.

Of course, if you want to avoid all of this confusion you can give to MLR before January 1st!

From everyone at Minnesota Lakes and Rivers, have a great holiday season and happy new year!

Thank you to the Association of Fundraising Professionals for their guides on this topic. Their articles can be found here.